2026 Investors Sentiment & Outlook

AVCA’s 2026 Investors Sentiment & Outlook report offers forward‑looking perspectives from Limited Partners (LPs) and General Partners (GPs) on Africa’s private capital markets.

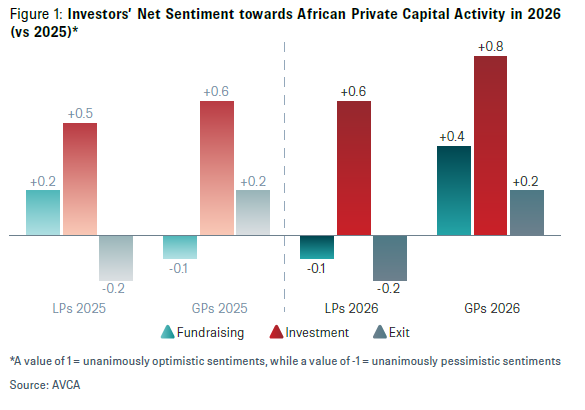

The findings point to a market characterised by strengthening conviction around investment activity, alongside continued caution on fundraising and exits. Improving dealmaking sentiment is underpinned by stronger pipelines, more attractive entry valuations and stabilising macroeconomic conditions, even as liquidity constraints persist.

For questions or comments on this publication, please contact research@avca.africa.

AVCA Members

Download the ReportNon-AVCA Members

Download the ReportBecome an AVCA member to unlock full access to the comprehensive survey findings from the report.

Key Findings

-

Deployment conviction is strengthening, even as liquidity remains constrained

Both LPs and GPs expect an active deal environment in 2026, supported by improving sentiment, stronger pipelines, and more attractive entry valuations. -

Liquidity, not opportunity, remains the binding constraint

Challenging exit conditions and slower capital recycling continue to weigh on fundraising and allocation pacing, driving more disciplined portfolio strategies. -

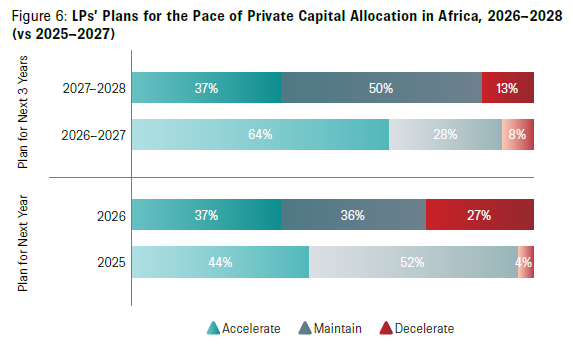

Long‑term commitment remains resilient despite near‑term caution

While 27% of LPs expect to slow commitments in 2026, 87% plan to maintain or increase allocations over the next three years, underscoring continued confidence in the asset class.

- Return performance is improving, supporting higher distribution expectations

A growing share of LPs and GPs reported double‑digit net IRRs in 2025, underpinning expectations of stronger distributions as portfolios mature. - Private credit is moving from complementary to strategic

Investors are increasing allocations to private debt, reflecting its role in providing income visibility, downside protection, and alignment with prolonged exit timelines. - Africa’s private capital ecosystem is becoming more locally anchored

Rising participation from African institutional investors is reinforcing long‑term capital commitment and contributing to a structurally more resilient market.